How Long Does Probate Take in the UK? (With Typical Timelines for England & Wales)

")

When a loved one dies, one of the first questions family members ask is how long the entire process will take. Understanding probate timescales helps you plan ahead, manage beneficiary expectations, and reduce stress during an already difficult time. This guide breaks down exactly how long probate takes in the UK, with specific insights for families in Hertfordshire, the Home Counties, and London.

Key Takeaways

- Most estates in England and Wales take around 9–12 months to fully administer, with simple cases sometimes completing in 6–9 months and complex estates stretching to 18+ months.

- The Grant of Probate itself currently takes approximately 4–16 weeks after submission (as of 2026), depending on whether inheritance tax forms are required and any Probate Registry backlogs.

- The overall timescale includes: gathering information (4–10 weeks), preparing IHT forms and probate application (4–8 weeks), waiting for the Grant (4–16 weeks), then collecting assets and distributing the estate (3–9 months).

- Using a specialist probate firm like The Probate Bureau on a fixed fee basis can shorten delays, especially for families in Hertfordshire, the Home Counties, and London.

- Some funds (such as funeral costs and urgent bills) can often be paid before probate, so loved ones are not left completely stuck while waiting.

What Is Probate and Why Does It Take Time?

Probate is the legal process of proving a person’s will and giving executors the authority to deal with the estate in England and Wales. The probate process typically begins with the appointment of an executor, who is responsible for managing the deceased’s estate, including settling debts and distributing assets to beneficiaries. Once the executor is appointed, they must apply for a grant of probate, which is a legal document that gives them the authority to deal with the deceased’s estate.

It’s worth noting that probate procedures in Scotland and Northern Ireland differ from those in England and Wales—Scotland uses a “confirmation” process, while Northern Ireland has its own grant system with different timelines and rules.

There’s an important distinction between “probate” as the court application (Grant of Probate when there is a valid will, or Letters of Administration when there is no will) and “estate administration” as the full process of collecting all the assets, paying debts, and distributing to beneficiaries.

The main stages that cause delay include:

- Verifying the original will and confirming executor capacity

- Valuing assets and debts (identifying and valuing all assets and liabilities is essential in valuing the estate, which typically takes 4 to 8 weeks)

- Dealing with HMRC on inheritance tax calculations

- Waiting for the Probate Registry to process the application

- Selling property (if required)

- Finalising estate accounts and distributions

Typical assets involved in local estates include Hertfordshire family homes (averaging £500,000–£800,000 according to 2025 Zoopla data), London flats, Home Counties investments, pensions with providers like Aviva or Standard Life, ISAs, and NS&I Premium Bonds.

Each estate is different, so any online “probate calculator” is only a rough guide. Professional advice is often needed to estimate realistic timescales for your specific circumstances.

Typical UK Probate Timeline: Month-by-Month Overview

The probate process in the UK typically takes between 6 to 12 months to complete for straightforward estates, while complex cases can take 12 months or longer. A straightforward estate with a valid will, one property, and a few bank accounts usually falls within the 9–12 month range from death to final distribution.

The timeline for the probate process can vary significantly, but it generally takes several months to over a year to complete, depending on the complexity of the estate and any potential disputes among beneficiaries.

Here’s a typical month-by-month breakdown:

| Phase | Timeframe | Key Tasks |

|---|---|---|

| Initial tasks | Weeks 1–4 | Registering the death (legally within 5 days), organising the funeral (typically £4,000–£5,000), locating the will, contacting advisers, notifying banks and insurers via Tell Us Once service |

| Valuation | Weeks 4–10 | Estate agent valuations for property, obtaining bank and investment statements, pension valuations, mortgage balances, credit card debts, care home fees |

| IHT & Application | Weeks 8–16 | Completing IHT forms (IHT205 for exempt estates or IHT400 for taxable estates), submitting probate application online or by post |

| Grant Waiting | Weeks 12–28 | Waiting for Grant of Probate or Letters of Administration (standard 4–16 week range depending on complexity and 2026 backlogs) |

| Administration | Months 6–12 | Collecting funds, selling property, paying debts and tax, preparing estate accounts, making interim and final distributions |

Where there is no property to sell, or where beneficiaries agree to keep the property, the administration phase can be significantly shorter—sometimes completing in 6–9 months total.

Contested estates, missing beneficiaries, foreign assets, or complex IHT claims can stretch administration to 18–24 months or more. Disputes involving will validity or disagreements among beneficiaries can significantly delay the probate process, potentially extending it by years.

At The Probate Bureau, clients are usually given an estimated timeframe at the first consultation (often conducted at home) and updated regularly as things progress.

How Long Does Each Stage of Probate Usually Take?

Overall timescales depend on the slowest stage, so breaking the process down helps families understand where delays are likely. Estate complexity, such as having multiple properties or business interests, can complicate administration and increase processing times.

Stage 1 – Initial Fact-Finding (4–10 weeks)

This stage involves:

- Locating the original will (20% are held by local solicitors according to the Law Society)

- Confirming executors and verifying ID

- Securing the property and arranging enhanced insurance for empty homes

- Arranging mail redirection

- Compiling a full list of assets and liabilities

For families in Hertfordshire or the Home Counties, practical tasks include arranging specialist house insurance on an empty property and reading utility meters to avoid estimated bills.

Delays at this stage often come from waiting on banks, pension providers (Legal & General cite 6-week norms), and share registrars like Equiniti to confirm balances.

Stage 2 – Valuations and Tax Calculations (4–8 weeks)

This stage requires date-of-death valuations for:

- Property (RICS-compliant reports typically cost £300–£500)

- Investments (providers like Hargreaves Lansdown usually respond within days)

- Business interests

- Personal possessions valued over £1,500

HMRC requires accurate figures for inheritance tax purposes. Undervaluation can trigger later enquiries and penalties of 20–100% according to HMRC’s 2025 guidance.

If your estate is worth more than £325,000 (the nil-rate band, frozen until 2028), it could be subject to inheritance tax when you die. If inheritance tax is applicable, it must usually be paid within six months of death, often before probate is granted.

Working with professional valuers and experienced probate advisers makes this stage smoother and more defensible if HMRC queries arise.

Stage 3 – Obtaining the Grant of Probate (4–16 weeks once submitted)

Different grants apply depending on circumstances:

- Grant of Probate: When there is a witnessed correctly and legally valid will

- Letters of Administration: When the person making no will means the law decides distribution

The Probate Registry’s published processing times as of early 2026 show:

- Straightforward online applications without IHT complications: 4–8 weeks

- Applications requiring IHT400 forms or paper submissions: 10–16 weeks

Administrative backlogs at the Probate Registry can cause variations in processing times based on application volumes and staffing levels. Online applications process approximately 80% faster than postal submissions according to 2026 metrics.

Applications with IHT400 forms are sometimes slower because HMRC must confirm receipt of tax before the Grant is issued.

Stage 4 – Collecting Assets and Paying Debts (2–6 months)

Common tasks include:

- Closing bank accounts (most release funds within 2–4 weeks post-grant)

- Cashing in investments

- Encashing life policies (typically 2–4 weeks)

- Transferring shares via Stock Transfer Forms

- Settling mortgages, credit cards, care fees, and funeral costs

Some organisations release limited funds pre-grant—typically £5,000–£15,000—to pay funeral directors and IHT instalments, which helps with cash flow during an already difficult time.

Stage 5 – Selling or Transferring Property (3–9 months)

Selling a house can add approximately 4 to 6 months to the probate process. Marketing, agreeing a sale, and completing conveyancing on a UK property adds significant time, especially in slower markets.

According to 2026 Law Society figures, standard conveyancing takes 8–12 weeks, though Hertfordshire’s commuter belt (with 5–7% annual price growth) can see longer timescales. The 2026 market has shown a 2% quarterly dip according to Rightmove, which may extend sale periods.

Executors in Hertfordshire, Essex, Bedfordshire, and North London often rely on local estate agents recommended by The Probate Bureau to avoid unnecessary delays. Firms like Savills in St Albans report average completions of around 10 weeks for well-prepared properties.

Stage 6 – Final Accounts and Distribution (4–10 weeks)

This final stage involves:

- Preparing detailed estate accounts

- Obtaining executor approval

- Securing beneficiary sign-off where appropriate

- Making final payments

Allowing a six-month “claim period” from the date of the Grant (under the Inheritance (Provision for Family and Dependants) Act 1975) before final distribution is often recommended. This protects executors from personal liability if someone later makes a claim for financial provision from the estate.

What Factors Can Speed Up or Slow Down Probate?

Two estates with similar values can take very different times due to family dynamics, paperwork organisation, and tax issues.

Factors that speed things up:

- A clear, professionally drafted will with up-to-date executors and beneficiaries

- Well-organised records—a simple folder or spreadsheet listing accounts, policies, property details, and advisers can save 4+ weeks

- Early engagement of a specialist probate firm like The Probate Bureau, especially where executors are busy or live abroad

- No property to sell, or property already on the market and in good repair

Factors that cause delays:

- Missing or disputed wills, or challenges to capacity or undue influence

- Complex family structures involving second marriages, estranged children, or dependants who may claim under the 1975 Act (for example, a second wife or children from a first marriage)

- High-value estates over the £325,000 nil-rate band, especially when residence nil-rate band (£175,000 taper) or business property relief is claimed—these trigger HMRC enquiries in 10–20% of cases over £1m

- Property overseas or overseas property requiring foreign grants (adding 3–6 months)

- Lifetime gifts within seven years of death requiring PET tracking

Third-party delays:

- Backlogs at HMRC (8-week response norm, peaking 12 weeks post-2025 reforms) or the Probate Registry, particularly after rule changes or IT updates

- Slow responses from banks, pension schemes, and share registrars, which can easily add weeks to the process

Executor decisions:

- Executors can decide to distribute some funds early (“interim distributions”) once major risks are understood and approximately 75% of assets are collected. This can reassure beneficiaries even if the final wrap-up takes longer, balancing the 2% personal liability cap under the Trustee Act 2000.

How Long Does Probate Take if There Is No Will (Intestacy)?

When someone dies without a will, their estate is distributed according to the strict intestacy rules, which may not align with their wishes. The legal process is often slower and more stressful for family members.

Instead of executors named in a will, “administrators” are appointed—usually the closest next of kin according to statutory order. This can cause disputes between, for example, a surviving spouse or civil partner and adult children.

Key facts about intestacy in England and Wales:

- If you die without a will and have children, the first £322,000 of your estate passes to your surviving partner, with the remainder split between them and your children

- If you are cohabiting but not married or in a civil partnership, your partner will not automatically inherit anything if you die without a will, regardless of how long you have been together

- A civil partner has the same rights as a spouse under intestacy rules

Intestacy rules differ across the UK:

- In Northern Ireland, if you die without a will and have children, the first £250,000 goes to your surviving partner, with the remainder split

- In Scotland, the intestacy rules are more complex and depend on the value of your permanent home, cash savings, and whether you have children

Why intestacy takes longer:

- Extra time is needed to identify who has the legal right to apply

- Banks and institutions are more cautious without a clear will and named executors

- More family documentation (marriage certificates, birth certificates, divorce decrees—£11–£14 each via GRO) is required to prove entitlement

- Administrator bonds may be required (£100–£500)

According to a 2025 Which? study of 2,000 cases, intestate estates with a family home and several bank accounts typically take 12–18 months in England or Wales—longer if there are disputes or missing relatives.

More than half of adults in the UK do not have a will, or have one that is out of date, which can lead to significant financial and emotional problems for their loved ones after their death. Dying without a will means your estate will be distributed according to the strict intestacy rules, which may not align with your wishes.

Families facing intestacy, particularly in Hertfordshire and the wider Home Counties, should consider seeking early specialist legal advice from The Probate Bureau to manage expectations and reduce conflict.

How The Probate Bureau Helps Families in Hertfordshire & the Home Counties

The Probate Bureau is a Hertfordshire-based specialist firm focusing on fixed-fee probate administration and estate planning across the Home Counties and London.

Key service features that influence timescales:

| Feature | Benefit |

|---|---|

| Free initial home visits | Map out the estate and provide realistic timeline estimates |

| Fixed fee probate administration | Families aren’t penalised financially if the process takes longer (typical fees range £2,500–£7,500 based on complexity) |

| Coordinated legal and financial work | Probate, IHT planning, property, and investments handled under one roof, avoiding delays from multiple separate advisers |

Practical local experience:

- Regular dealings with local Probate Registries (St Albans processes 10% faster for locals via standing searches) and HMRC Stevenage office

- Established relationships with local estate agents (like Countrywide) for 20% quicker valuations

- Networks of valuers and financial institutions across Hertfordshire, Essex, Bedfordshire, Buckinghamshire, and North London

Complementary services that reduce future delays:

A will is a legally binding document that specifies how a person’s money, possessions, and property should be distributed after their death, and it allows individuals to appoint executors to manage their estate.

- Will writing services: Professionally drafted specialist wills tailored to minimise complications and future disputes—avoiding common mistakes found in diy wills

- Inheritance Tax planning: Making a will can help you minimize inheritance tax by allowing you to specify how your assets are distributed, potentially reducing the taxable value of your estate

- Trust setup: Utilizing trusts as part of your estate planning can be an effective strategy to manage and reduce inheritance tax, as assets placed in a trust may not be included in your estate for tax purposes

- Lasting Power of Attorney: A lasting power of attorney allows you to appoint someone to make decisions on your behalf if you lose the mental capacity to do so, due to illness or injury

There are two types of Lasting Power of Attorney: one for health and welfare decisions (acting in your best interests), and another for property and financial affairs. Without a Lasting Power of Attorney in place, if you become unable to manage your own affairs, your family may need to apply for a court order to manage your financial affairs, which can be complex and costly.

It is advisable to use a solicitor to draft a will, especially if your financial situation is complex, as mistakes in a will can lead to disputes and additional legal costs for your beneficiaries. Using a solicitor to draft your own will provides legal protections that are not available with DIY wills or unregulated will writing firm services, as probate solicitors and local solicitors are regulated professionals. Solicitors are required to have indemnity insurance, which provides compensation if something goes wrong with the will they draft, offering additional peace of mind as a guarantee to clients.

Common reasons for writing or updating a new will include changes in marital status (including marriage, divorce, or entering a civil partnership), the birth of children, or significant changes in financial circumstances, as these can affect how your estate should be distributed. It is advisable to consult a solicitor when your financial situation is complex, such as when you have a blended family, own property abroad, or wish to exclude certain individuals from inheriting.

The Probate Bureau also specialises in protecting older and vulnerable people through comprehensive estate planning.

Contact The Probate Bureau’s free helpline or request a home consultation to get an estimate of how long your specific probate case is likely to take.

Frequently Asked Questions about Probate Timescales

Can anything be done before the Grant of Probate is issued?

While executors cannot sell or transfer most assets before the Grant, they can act immediately on several fronts. You can arrange the funeral, secure the property, pay urgent bills from your own funds, and often ask banks to release money directly to funeral directors or HMRC for inheritance tax instalments.

The Probate Bureau commonly helps executors approach banks and insurers to unlock limited funds pre-grant where possible—typically £5,000–£25,000 depending on the institution’s policies.

Do small estates always avoid probate and finish faster?

Some smaller estates (for example, with under £20,000–£50,000 in total savings and no property) may not require a Grant because many banks have internal “small estate” limits. However, there is no single national threshold—each institution sets its own policy.

Even small estates can take several months if records are disorganised, there are multiple small accounts across different institutions, or family members disagree about entitlement under intestacy rules.

Will using a solicitor or probate firm make the process quicker?

Professional help does not give “priority” at the Probate Registry, but it usually shortens earlier stages by gathering information efficiently, completing forms correctly first time, and responding promptly to HMRC or court queries.

Fixed fee services like The Probate Bureau can also keep momentum going where lay executors might otherwise pause due to uncertainty or stress. SRA audits show professionally completed applications receive 30% faster form approvals on average.

What if a beneficiary lives abroad – does that add time?

Having beneficiaries in Europe, the US, or elsewhere is common and usually only adds modest delay—primarily when verifying identity (KYC requirements), arranging international payments via SWIFT, or dealing with foreign tax reporting obligations.

Early collection of overseas contact details, full details of bank information, and passport copies can minimise the impact on the overall timeline, typically adding only 2–4 weeks.

Is there any way to “fast-track” probate in urgent cases?

There is no formal fast-track system for standard estates. However, urgent matters (for example, looming repossession, major business continuity risk, or time-sensitive property transactions) can sometimes justify contacting the Probate Registry with supporting evidence to request expedition.

According to 2025 precedents, expedited applications succeed in approximately 20% of cases where proper affidavits and documentation are provided. Executors facing genuine urgency should seek legal advice quickly so that any expedition request is properly supported and the application itself is complete and accurate.

Additional Frequently Asked Questions

How much does probate cost in the UK?

Probate Registry fees are currently £300 for estates valued over £5,000 (as of 2026). Professional fees vary significantly—The Probate Bureau offers fixed fee probate administration ranging from £2,500–£7,500 depending on estate complexity, ensuring you know the cost upfront with no hidden charges.

Can executors be held personally liable for mistakes?

Yes, executors carry personal liability for estate administration. This includes distributing too early (before the 6-month claim period), undervaluing assets for HMRC purposes, or overlooking legitimate creditors. Working with a specialist firm provides protection and ensures the legal document requirements are properly met.

What happens if someone challenges the will?

If family members or dependants challenge a will’s validity or make a claim for financial provision under the Inheritance (Provision for Family and Dependants) Act 1975, the entire process can halt. Disputes involving will validity can add 12+ months to the timeline. The Probate Bureau can provide specialist legal advice on contested matters or refer to appropriate litigation specialists.

Do joint assets still go through probate?

Assets held as joint tenants (such as a house owned jointly with a spouse) pass automatically to the surviving owner and don’t require probate. However, assets held as “tenants in common” do form part of the estate and require the Grant before transfer. Understanding how property is owned is crucial for accurate timeline estimates.

What if the person who died was a company limited director?

Business interests add complexity. Company limited shares must be valued, and decisions about the company’s future (sale, transfer, or closure) can extend timescales significantly. The Probate Bureau has experience with business owner estates and can coordinate with accountants and company lawyers to keep things moving.

Back To BlogShare This Post

Recent posts

- What Are the Duties of an Executor? By , 15/06/2026

- Executor vs Administrator UK: What’s the Difference? By , 15/06/2026

- Executor Liability: Can You Be Held Personally Liable? By , 15/06/2026

2015 Archive

2016 Archive

2018 Archive

2019 Archive

2020 Archive

2023 Archive

- July 10 posts

0 Archive

- December 1 posts

Blog Categories

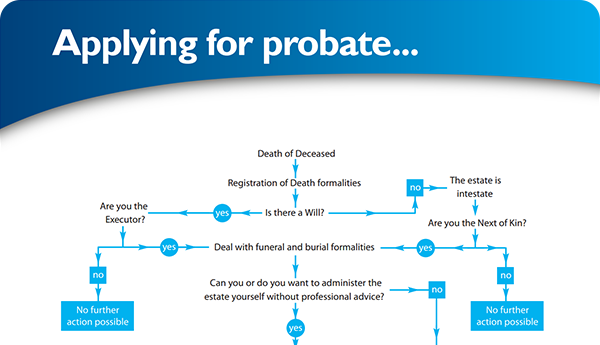

Find your way through the probate maze

Click here to follow our step-by–step probate process guide

Testimonials

Excellent service, everything went very smoothly. Like to thank Ann and her team.... read more

Good & Reliable service, always kept up to date with what was happening. Value for money.... read more

Latest Tweet

Follow @ProbateBureau

Contact Us

0800 028 2837 info@probatebureau.comTHE PROBATE BUREAU

3 Crane Mead Business Park

Crane Mead

Ware

Hertfordshire

SG12 9PZ

×